In December 2020, I published Innovation Casino, a book about how medium-sized and large enterprises can use corporate venture capital (CVC) to grow their digital ecosystems. Here, you can read a chapter-by-chapter summary.

What’s in it for me? Beat the odds with CVC for digital ecosystems.

The book, Innovation Casino, uses its self-titled metaphor to describe the odds of generating financial returns from innovation so you can beat them. For decades, vertically integrated firms have made high-stakes bets on innovation. However, in the innovation casino, it is the players who bet big. Players think they will beat the odds, but few do. By taking a fresh look at your odds, you can retool your approach to win more frequently just as the house does in a casino.

Large firms have a unique opportunity to improve their odds in the innovation casino with an emerging business model called “digital ecosystems.” Digital ecosystems give large firms the opportunity to make thousands of bets on innovation, which is playing like the house. Each chapter in this book provides a “house strategy” to fund non-core innovation in digital ecosystems:

- Fund startups instead of acquiring companies

- Master the odds to invest in startups

- Recoup principal with 100X more bets than VC

- Standardize to deliver gains from overall performance

Core Innovation: Improving your core offerings

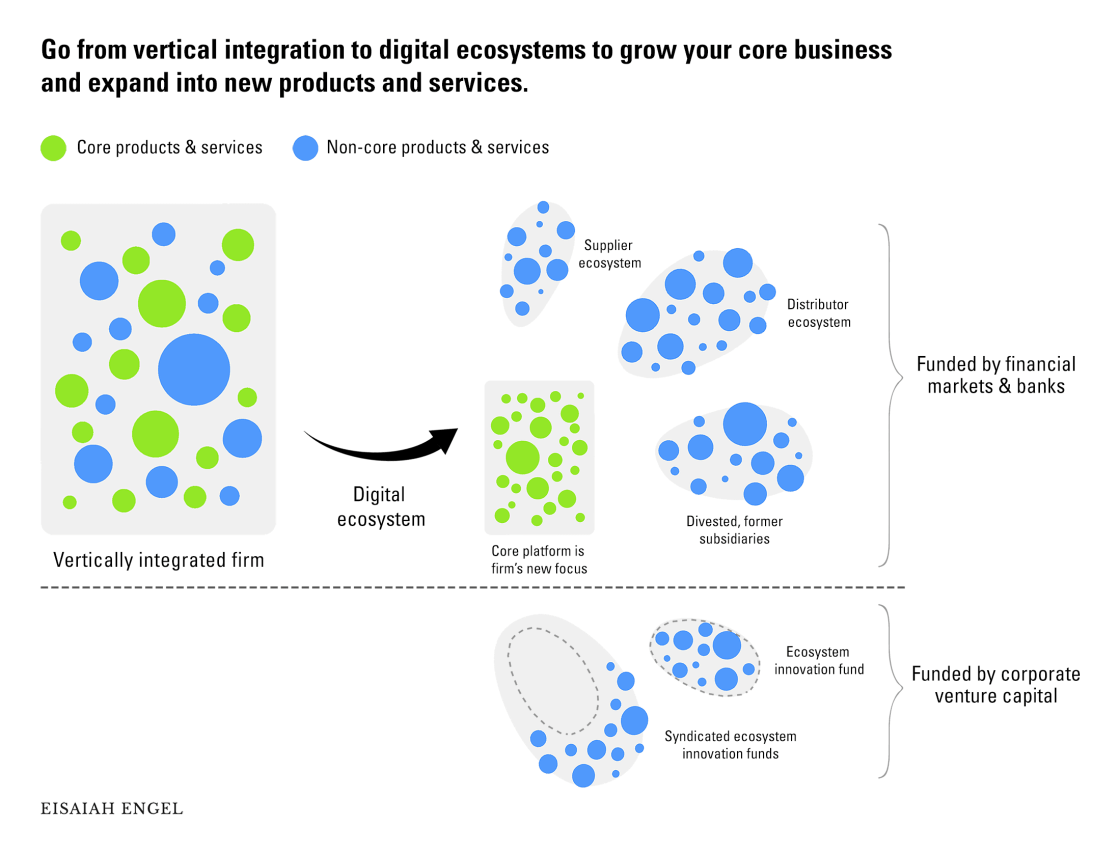

Core products and services are at the center of your company’s skill set and reason for existing. Like the Apple iPhone or the Amazon Web Services platform, core offerings can become platforms for other companies to extend. You should focus your resources for research, development, and acquisitions on refining and transforming your core offerings.

Non-Core Innovation: Improving your non-core offerings

Non-core products and services are not at the center of your company’s skill set and reason for existing. Non-core offerings may drive demand for your core offerings, which can make it temping to devote teams and budgets to them. However, Innovation Casino proposes you fund promising non-core ideas with an ecosystem innovation fund, or EIF, which you will read about later in this summary.

Like the “app store” on your phone, a digital ecosystem is a supply chain for data and digital services that are delivered over a platform. A digital ecosystem has three components: (1) a platform, (2) network effects, and (3) market expectations of continued growth. An example that checks all three boxes is the Apple App Store. At the end of 2019, the Apple App Store had 1.84 million apps. Apple is playing the innovation game like the house because it only makes a handful of the apps that reside on its platform. The rest of the 1.84 million apps were built by developers, and Apple reaps the financial rewards by housing them.

By contrast, BlackBerry developed a rival app store called “BlackBerry World.” BlackBerry World could not rival the network effects Apple was generating between developers and customers. The market increasingly expected BlackBerry World to fall behind. Its death spiral ended in 2019 when BlackBerry World was shut down. Using the above definition of a digital ecosystem, Blackberry checked the box for having a platform but fell short when it came to generating network effects and market expectations.

BlackBerry World typifies the challenge in building digital ecosystems: growing network effects between outside developers and customers. The solution is to give customers and developers more reasons to use your platform. This can be done by combining open innovation with seed funding, so outside startups—not internal teams—build thousands of new products and services that drive demand for your core products.

Innovation Casino proposes a new corporate venture capital strategy that transfers the approach of the US government’s Small Business Innovation Research (SBIR) program. As a grant program, SBIR is missing a way to generate returns. Venture capital fills this gap by making equity investments and raising capital from outside investors. To describe such a hybrid fund, this book introduces the term ecosystem innovation fund, or EIF. A large company with an EIF can become the house in the innovation casino by funding startups in its digital ecosystem with outside capital, returning principal from these investments, and delivering gains from its stock price.

The key message here is: The term “innovation casino” is a metaphor for the odds of generating financial returns from innovation. Digital ecosystems give your large firm the opportunity to make thousands of bets on non-core innovation, which is playing like the house. To play like the house, use a new type of corporate venture capital fund called an EIF.

House Strategy 1: Fund Startups Instead of Acquiring Companies

Even before COVID-19, US government debt was nearing all-time highs. The pandemic response compounded public debt to levels not seen since World War II. To restore public finances, the US government will need to raise taxes. Higher taxes will erode cash flow at a time when corporate debt is high. Having less cash flow will reduce credit quality and make borrowing more expensive. Companies seeking to deliver outsized returns will need to grow organically rather than via mergers and acquisitions.

Growing organically means that businesses will need to find new reasons for customers to pay a premium, remain loyal, and refer friends. To do so will require companies to tap their innovative powers and improve their core assets by 10X. Standing in the way is the fact that many large companies spent the last decade acquiring non-core assets. A non-core asset is not central to the service a company provides. For example, when Microsoft bought the devices and services business of Nokia in 2013, it acquired a non-core asset. Non-core assets can be good when they drive demand for your core business. But having them under one roof can distract from innovation and create sprawling bureaucracy. In a world of digital ecosystems, a non-core asset can be divested while remaining connected to customers through its former parent’s platform. That way, there is no interruption to the end customer.

Ideas for new, non-core assets can be funded with an EIF. The rest of this book is about becoming the house in the innovation casino with an EIF that uses cash from outside investors and returns principal and gains from ecosystem performance.

The key message here is: The business environment in the decade following COVID-19 will be saddled with debt and higher taxes. Companies will need to change course—focusing on core assets and moving non-core innovation to their digital ecosystems. In a digital ecosystem, non-core ideas can be funded with an EIF, which is new type of corporate venture capital fund.

House Strategy 2: Master the Odds to Invest in Startups

Venture capital (VC) fund returns are the closest proxy we have to calculate the odds of generating financial returns from innovation. There are three reasons why:

- VC bets on young companies whose fortunes correlate to innovation, since they are often too young to have mature product portfolios.

- VC funds typically bet on less than 20 companies; when one investment succeeds, the fund can post positive returns.

- There are no other large datasets that directly measure financial returns on investments from innovation.

This book uses a dataset, compiled by PitchBook, of 827 VC funds established between 1976 and 2008, with performance data through January 2019.

Pitchbook data of Distribution of Paid in Capital (DPI) reveal the break-even point where investors in VC funds get their cash back is the 48th percentile. At the same percentile, fund IRR equals 4.4%. This discrepancy between the break-even points of DPI and IRR suggests IRR is not accounting for costs, and the costs of running a VC fund are 4.4% per year. So, this book adjusts the power curve of VC returns down by 4.4% and calls the adjusted values “Historical VC Returns.”

Historical VC Returns form a base case for a company’s odds in the innovation casino:

- Just over 2 in 10 investments in innovation will beat the US stock market.

- Just over 1 in 2 investments in innovation will recoup principal.

- Just under 4 in 10 investments in innovation will lose more than a quarter of principal.

The key message here is: VC odds show a base case for how an EIF could perform. The VC risk/reward ratio is ideal for players in the innovation casino, but the odds are this way because VC concentrates its bets on just a handful of companies. To play like the house, an EIF must diversify.

House Strategy 3: Recoup Principal with 100X More Bets than VC

One way for an EIF to make 100X more bets than a typical VC fund is to pool with other EIFs. This book simulates 100 EIFs each making 20 investments—the number of investments typical VC funds make—and pooling 50% of each investment to gain exposure to 2,000 startups.

Pooled EIFs do not need to be as skilled at selecting investments as VC, and indeed, they are not. When separated from the pool, EIFs are 35% more likely to lose principal than Historical VC Returns. Yet, none of the same EIFs lose principal when they are pooled. This difference speaks to the power of diversification to preserve principal.

A VC fund or EIF that loses principal is likely to exit the game early. Simulated 500 times, Historical VC Returns fluctuate from -13.1% to 23.8% IRR while pooled EIFs consistently return principal between 2.3% and 13.8% IRR.

EIFs need to standardize their investment processes and criteria. This serves two purposes:

- Recoup principal by enabling EIFs to pool investments with each other using a common framework

- Build a thriving digital ecosystem with investments that accomplish corporate innovation objectives

The key message is: Investment processes and criteria can be used to diversify an EIF to the point where it nearly always returns principal. The same processes and criteria can help build a strong digital ecosystem.

House Strategy 4: Standardize to Deliver Gains from Overall Performance

Outside investors can capitalize your EIF, freeing up your parent company’s cash flow. Your EIF must return principal and gains. The previous chapter shows how to return principal by diversifying. This chapter is about driving gains. Outside EIF investors would receive warrants on your parent company’s stock, so they can gain when the share price goes up due to digital ecosystem success. Depending on what the stock market does, EIF investors can receive liquid gains sooner than typical VC investors.

To build a strong ecosystem, EIF processes and investment criteria must be standardized and honed. Here, companies can learn from the US government’s Small Business Innovation Research (SBIR) grant program. SBIR is perhaps the first funding program designed to achieve both innovation and ecosystem objectives. SBIR has helped generate 70,000 patents, start nearly 700 publicly traded companies, and raise around $41 billion in VC investments since its inception in 1982.

EIFs should adopt three practices from SBIR to align funding with corporate innovation and ecosystem outcomes:

- Work with startups: SBIR discovered that startups outperform established small businesses in delivering new products and services that customers want.

- Take an outside view: Keep your funding requirements flexible so startups can take approaches that were not considered by your internal teams.

- Commercialize early: Require startups to maintain marketing and follow-on financing plans from the beginning when they apply for funding.

As a grant program, SBIR is missing a way to generate returns. VC fills this gap by making equity investments and raising capital from outside investors.

An EIF is a new way to do corporate venture capital, or CVC. The best practices of SBIR and CVC already resemble each other. Thus, the programs can be remixed into the new approach of the EIF.

| Best practices of SBIR and CVC | SBIR | CVC |

| % of parent company or agency R&D budgets | 3.2% | 4% |

| Balances innovation with commercialization | ✓ | ✓ |

| Focuses on strategic value first and then financial returns | ✓ | ✓ |

| Provides distribution and support for the start-ups they fund | ✓ | ✓ |

EIFs are a type of CVC fund best suited for “zebra” startups. The term zebra was introduced in 2017 by Zebras Unite, an organization calling for a more ethical and inclusive alternative to VC culture. Zebra startups focus on serving a niche. Many of the companies on the Inc 5000 list are zebras. Zebra startups differ from so-called “unicorn” companies, which VC culture tends to focus on: companies such as Facebook, Instagram, Twitter, Uber, and Airbnb. Unicorn companies often grow quickly and unprofitably with the hopes of raising prices down the road. Unlike their unicorn cousins, zebras are startups that aspire to grow profitably.

Your EIF can be a desirable source of funding for zebra startups with terms that let founders stay in control of their companies. VC deal terms contain investor protections that limit founders’ autonomy, which is documented in my 2019 study of popular VC term sheets. An EIF can stand out by adopting Founder Friendly Standard, a term sheet that gives entrepreneurs control of their companies. In exchange for offering founders unprecedented control, your EIF could undercut other VC firms and consistently buy low. Buying low is the number one driver of returns in venture capital. This practice could work for zebra startups because zebras only need small amounts of capital to reach profitable growth.

The key message is: An EIF can lift the stock price of your parent company by growing its digital ecosystem. Consistency is key. Transfer the approach of the SBIR grant program to consistently fund “zebra” startups that meet your innovation objectives. Use a Founder Friendly Standard term sheet to consistently buy low.

Final summary

The key messages in this summary are:

The term “innovation casino” is a metaphor for the odds of generating financial returns from innovation. Digital ecosystems give large firms the opportunity to make thousands of bets on innovation, which is playing like the house. The business environment in the decade following COVID-19 will be saddled with debt and higher taxes. Companies will need to change course—focusing on core assets and moving non-core innovation to their digital ecosystems. In a digital ecosystem, non-core ideas can be funded with an EIF, which is a type of corporate VC fund. VC odds show a base case for how an EIF could perform. The VC risk/reward ratio is ideal for players in the innovation casino, but the odds are this way because VC concentrates its bets on just a handful of companies. To play like the house, an EIF must diversify. Investment processes and criteria can diversify an EIF to the point where it nearly always returns principal. The same processes and criteria can help you build a strong digital ecosystem and thereby increase the value of your parent company’s stock. Consistency is key. Learn from the SBIR grant program to consistently fund startups that meet your innovation objectives. Learn from Founder Friendly Standard to consistently buy low, which is essential to driving returns.

Take this next step:

Categorize core and non-core assets to optimize digital ecosystem innovation

Begin the process at your company of categorizing assets as core and non-core. Non-core assets are likely preventing your organization from improving your core products by 10X. Explore with your team how non-core assets can be divested while remaining connected to customers through your core platform. Set up idea management software to capture new proposals and begin labeling them as core and non-core. Core ideas can be built by your internal teams while non-core ideas can eventually be funded by your EIF.

If you would like a copy of Innovation Casino, you can get it from Amazon here. Thank you for supporting my research about how corporate venture capital can spur digital ecosystem innovation.

Limit of Liability/Disclaimer of Warranty: The Author and the Publisher are not providing any financial, economic, legal, accounting, or tax advice or recommendations in this book. The information contained in this book was prepared for general information purposes only, does not constitute research, advice, or a recommendation from the Author and the Publisher to the reader, and is not a substitute for personalized financial advice. Neither the Author, the Publisher, nor any of their affiliates make any representation or warranty as to the accuracy or completeness of the statements contained in this book. The Author, the Publisher, and their affiliates expressly disclaim any liability (including any direct, indirect, or consequential loss or damages) for this book and its content.